In this guide, you will learn:

- what deed in lieu vs short sale houston best options means in practice;

- which inputs, rules, costs, or assumptions change the answer;

- the step-by-step decision process;

- the primary sources to check; and

- when to stop and ask a qualified professional.

The short answer

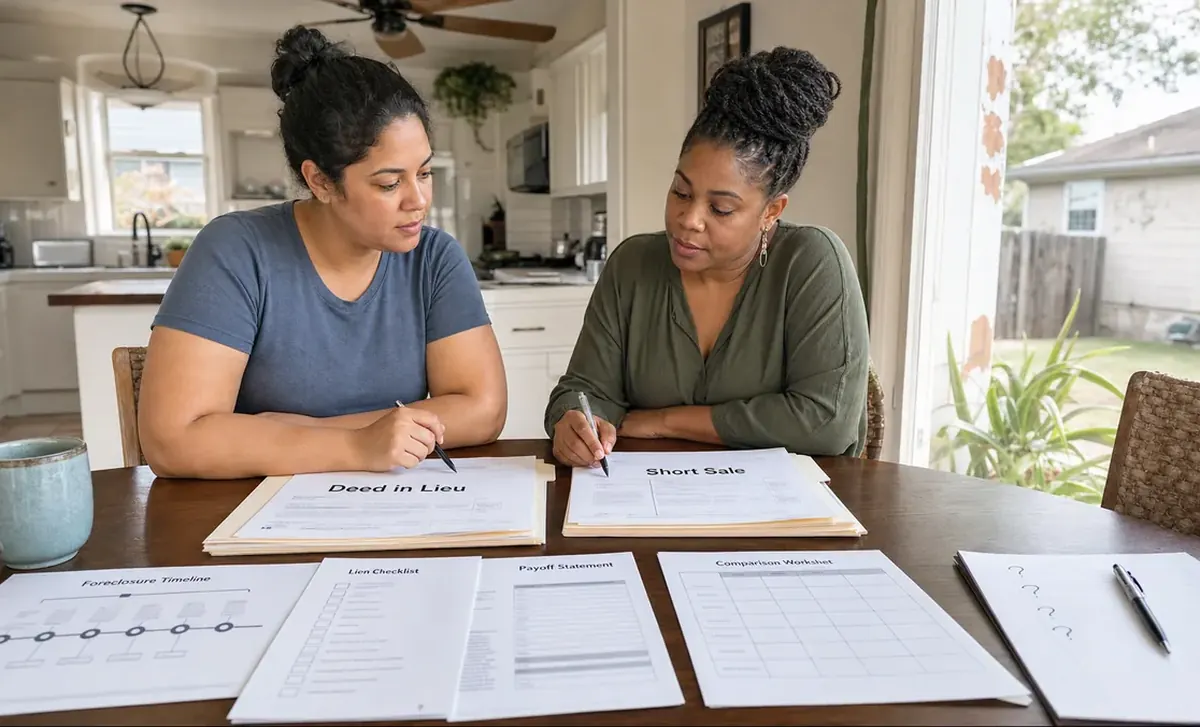

A deed in lieu and a short sale are different lender-approved loss-mitigation paths. In a deed in lieu, an owner voluntarily transfers the property to the lender or investor under a written agreement. In a short sale, the property is sold to a buyer for an amount that may be insufficient to pay every secured obligation and cost, so required parties must approve the transaction and closing terms.

Neither label establishes eligibility, postpones a foreclosure sale, waives a remaining balance, settles junior liens, determines tax treatment, guarantees credit reporting, or fixes a move-out date. The controlling documents are the current written notices, approvals, releases, contract, settlement statement, and recorded instruments for the specific file. Contact the mortgage servicer and a HUD-approved housing counselor promptly; ask a qualified Texas lawyer and tax professional to review legal and tax consequences.

Who this applies to

This guide is for Houston-area homeowners comparing a deed-in-lieu request with a short-sale request before a scheduled foreclosure or other deadline. It is educational, not a determination that either option is available or preferable.

Immediate professional review is warranted when a sale date is posted, bankruptcy is pending or contemplated, military-service protections may apply, probate or divorce affects authority, tenants occupy the home, title or liens are disputed, fraud is suspected, or a lender document contains deficiency, release, relocation, tax, credit-reporting, or possession language you do not understand.

Inputs and definitions

- Mortgage servicer

- The company that receives payments and administers the loan. It may act for another owner or investor whose rules affect available options.

- Deed in lieu of foreclosure

- A voluntary transfer accepted under written terms. Acceptance, title requirements, debt treatment, possession, and reporting are file-specific.

- Short sale

- A sale requiring approval when proceeds will not satisfy every required payoff and transaction cost under ordinary terms.

- Deficiency

- A potential remaining amount after collateral or sale proceeds are applied. Whether it exists or is released is a legal, contractual, and jurisdiction-specific question.

- Junior lien

- A lien with lower priority than another lien. Every required interest must be addressed for the proposed closing or transfer.

Step-by-step process

- Record the deadline. Obtain the current foreclosure notice and confirm the sale date and status directly with the servicer or trustee. Do not assume an application pauses action.

- Identify the decision-maker. Confirm the servicer, loan owner or investor where available, and the department handling loss mitigation.

- Build the file. Ask for the current application and exact document list. Submit through a verifiable channel and retain delivery records.

- Order title and payoff information. Identify mortgages, taxes, association claims, judgments, and other interests. Do not assume the first lender can release another party’s claim.

- Request written terms for each available path. Ask about approval conditions, required sale or transfer documents, deficiency treatment, subordinate interests, expenses, tax forms, credit reporting, possession, relocation terms, and deadlines.

- For a short sale, document the buyer path. Verify the contract, financing or funds, settlement estimate, property information, marketing evidence requested by the servicer, and all approval conditions.

- For a deed in lieu, document the transfer path. Verify title requirements, vacancy or occupancy terms, property condition, deed and release language, personal-property requirements, and effective date.

- Get independent review before signing. A housing counselor can help with process; qualified lawyers and tax professionals address legal and tax consequences.

- Compare the final written alternatives. Use the same effective date and do not count a verbal statement as a waiver, postponement, approval, or release.

Worked example with assumptions

Hypothetical workflow—not an eligibility or outcome prediction

Assume an owner has a current foreclosure notice, a servicer application, a preliminary title report, and a possible buyer. No property value, payoff, deficiency, approval period, credit result, tax result, or postponement is assumed.

Create two columns. In each, copy the servicer’s written requirements, outstanding liens, approval deadline, required documents, debt-release language, tax-form language, possession date, closing dependencies, and unresolved questions. Attach the source document and date to every entry. A housing counselor, lawyer, and tax professional can then review the actual file rather than a generic comparison.

Individual results vary. This example is not a promise that either option will be offered, approved, completed, or reported in a particular way.

Costs, risks, and common mistakes

- Assuming an application or verbal assurance postpones a scheduled sale.

- Treating a deed transfer, short-sale approval, debt release, and lien release as the same thing.

- Ignoring junior liens, association claims, taxes, judgments, probate, divorce, or bankruptcy authority.

- Signing a contract or deed before reviewing deficiency, release, possession, relocation, and tax-reporting language.

- Predicting approval speed, credit-score impact, forgiven debt, tax liability, or cash-at-closing without file-specific evidence.

- Paying an unverified foreclosure-rescue company or transferring title based on a pressure tactic.

- Comparing a direct offer with lender alternatives without confirming whether proceeds satisfy every required payoff and cost.

- Sending sensitive documents through an unverified email, portal, phone number, or wire instruction.

Rules or facts to verify now

CFPB’s short-sale explanation describes the general concept and directs borrowers to contact their servicer. CFPB’s deed-in-lieu explanation provides the corresponding general definition.

Texas Property Code §51.002 contains procedures applicable to certain sales of real property under contract liens. A qualified lawyer should determine the governing process and deadlines for your documents.

Review the IRS’s current Topic No. 431 on canceled debt and file-specific tax forms with a qualified tax professional. Report suspected rescue schemes using the FTC mortgage-relief scam guidance.

Primary sources

- Consumer Financial Protection Bureau: short sale.

- Consumer Financial Protection Bureau: deed in lieu.

- CFPB housing counselor finder.

- Texas Property Code §51.002.

- IRS Topic No. 431: canceled debt.

- Federal Trade Commission mortgage-relief scam guidance.

Frequently asked questions

Does applying stop a Texas foreclosure sale?

Do not assume it does. Confirm the current status and any postponement in writing with the servicer or trustee, and obtain prompt legal advice about your deadline.

Does either option automatically waive the remaining debt?

No automatic result should be assumed. Review the signed approval, release, closing statement, applicable law, and every lien with qualified counsel.

Which option has less credit impact?

This page does not predict credit reporting or scoring. Ask the servicer what it will report, retain the final documents, and consult a qualified credit or legal professional about your file.

Can a direct sale replace lender approval?

Not when sale proceeds and other funds cannot satisfy every required payoff and cost. The lender or other lienholder may still need to approve a short payoff or other arrangement.